Memory Spot Prices Rise More Slowly as Trading Pauses for Lunar New Year

Memory spot prices are still edging higher, but the pace has slowed as trading activity cools ahead of the Lunar New Year. In its latest weekly update, TrendForce said many buyers and traders are sitting on their hands, with fewer quotes and fewer deals being done.

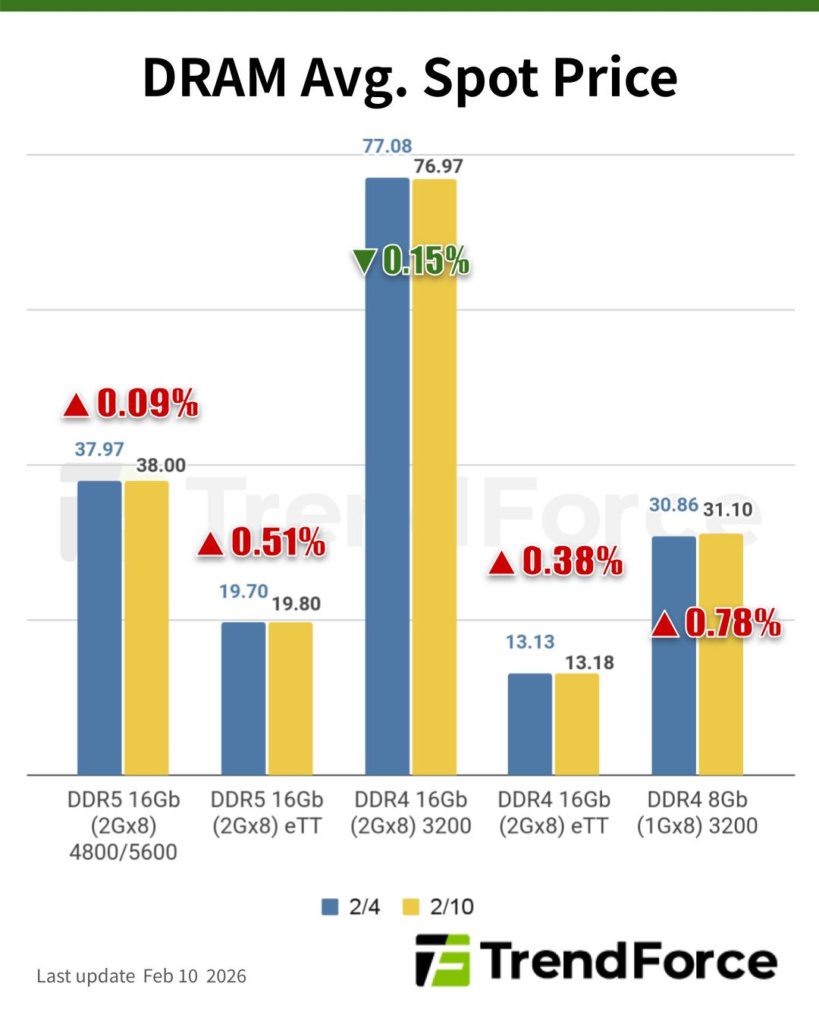

TrendForce’s DRAM average spot price chart shows mostly modest week-on-week moves between 4 Feb and 10 Feb 2026.

Memory spot prices cool as the spot–contract gap narrows

TrendForce’s core point is that spot levels have run well ahead of contract prices, so further near-term upside looks harder to sustain. In DRAM, it said the average spot price for a mainstream part (DDR4 1Gx8 3,200MT/s) rose by 0.78% week-on-week to $31.10. The expectation is for more modest moves if the market keeps treating spot pricing as “too far above” contract levels, allowing the gap to converge rather than widen further.

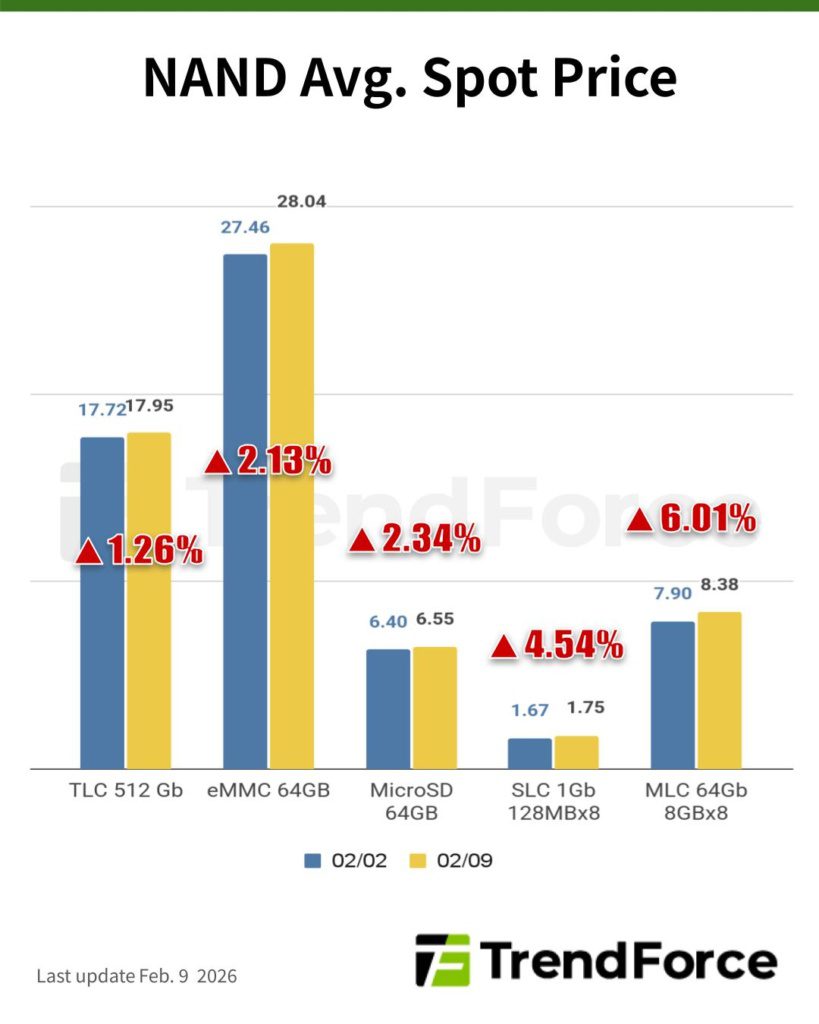

For NAND flash, TrendForce described holiday-related factory stoppages and already-elevated pricing as dampening purchase sentiment and reducing transactions. It reported spot prices for 512Gb TLC wafers rising 1.26% week-on-week to $17.948, alongside commentary that some traders are trimming inventory for cash ahead of the holiday, without materially shaking supplier confidence on pricing.

TrendForce’s NAND average spot price chart shows broad week-on-week gains between 2 Feb and 9 Feb 2026.

What this means for memory spot prices versus the bigger 2026 picture

A slower week in spot trading is not the same thing as the cycle turning. Contract markets remain the bigger driver for OEM bill-of-materials planning, and TrendForce has been projecting very large contract increases for early 2026 in both DRAM and NAND categories. That sits alongside broader, public commentary from major suppliers that AI-led demand remains strong through 2026 and into 2027.

In practical terms, “memory spot prices” cooling for a week or two (especially around a major holiday) mostly signals near-term digestion after a sharp run-up. For PC and device makers, the more important question is whether contract negotiations eventually pull spot down, or whether contract pricing keeps catching up to spot.

As previously reported by eeNews Europe when memory pricing momentum was accelerating, the industry has been bracing for substantial increases tied to tight supply, allocation discipline, and AI infrastructure demand. A quieter spot tape does not remove that pressure — but it may hint that the market is becoming more sensitive to how far spot can run ahead of contracts before buyers step back.

For a second independent reference point, DRAMeXchange continues to publish daily spot indications across DRAM and NAND items, and remains a useful sanity check for where spot levels are sitting day to day.

If you enjoyed this article, you will like the following ones: don't miss them by subscribing to :

If you enjoyed this article, you will like the following ones: don't miss them by subscribing to :