Memory price surge lifts Samsung, SK hynix and Micron

Memory prices are running hot again, with the latest forecasts pointing to steep quarter-on-quarter increases for both DRAM and NAND in early 2026. The dynamic is familiar: Hyperscalers and AI-server builders are soaking up supply, while manufacturers prioritise higher-margin server DRAM and high-bandwidth memory (HBM), leaving PC and handset buyers to fight over what’s left.

Memory price surge driven by AI capacity grabs

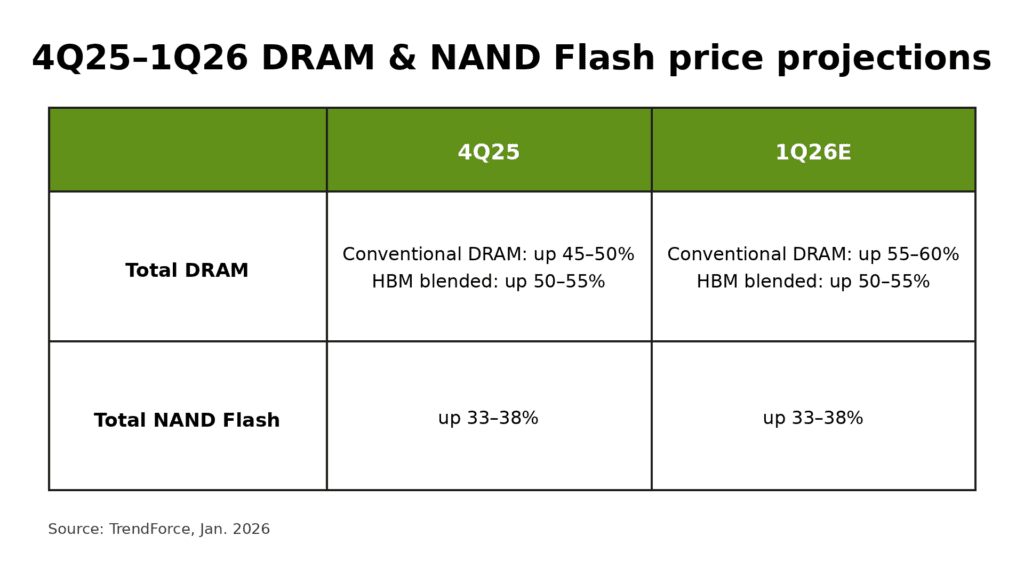

Market watcher TrendForce expects conventional DRAM contract prices to rise around 55–60% in Q1 2026, with NAND flash contract prices up about 33–38% over the same period. Within that, server DRAM is forecast to climb by more than 60% as US-based cloud service providers lock in capacity and supplier inventories tighten.

TrendForce projects further DRAM and NAND flash contract-price rises from 4Q25 into 1Q26E, led by conventional DRAM.

The knock-on effects are already showing up in company performance and guidance. Samsung is widely expected to post a sharp year-on-year jump in quarterly operating profit on the back of stronger memory pricing, while rivals including SK hynix and Micron continue to position HBM and server memory as the key profit engine for 2026.

What it means for PCs, phones and “normal” SSDs

For OEMs outside the AI gold rush, the problem is less about demand disappearing and more about being outbid. PC makers and module houses typically rely on steadier commodity DRAM flows, but when supply is constrained they can be forced into higher-priced channels. In practical terms, that can translate into awkward product decisions: smaller default RAM configurations, slower refresh cycles, and pricier upgrade SKUs (for example, moving a mainstream laptop from 16 GB to 32 GB becomes a noticeably more expensive step).

Handset makers face a similar squeeze. Even if smartphone demand is seasonally softer, tight LPDDR supply can keep pricing firm—particularly when leading-edge process capacity is being pulled towards server parts. On the storage side, enterprise SSD demand is increasingly tied to data-centre build-outs, and that can crowd out client SSD supply and keep NAND pricing elevated.

Supply discipline is back in fashion

After the industry’s previous boom-bust cycles, memory suppliers have been more willing to manage output and prioritise margins. The result is a market where pricing can move faster than device makers are comfortable with, and where the “memory price surge” story is increasingly linked to structural allocation decisions (HBM and server-first) rather than a short-lived hiccup.

As previously reported by eeNews Europe when price rises helped drive the memory markets sharply higher, the sector’s up-cycles can be abrupt when demand and supply planning fall out of sync.

For the latest Q1 2026 numbers, see TrendForce’s 1Q26 contract-price outlook.

If you enjoyed this article, you will like the following ones: don't miss them by subscribing to :

If you enjoyed this article, you will like the following ones: don't miss them by subscribing to :